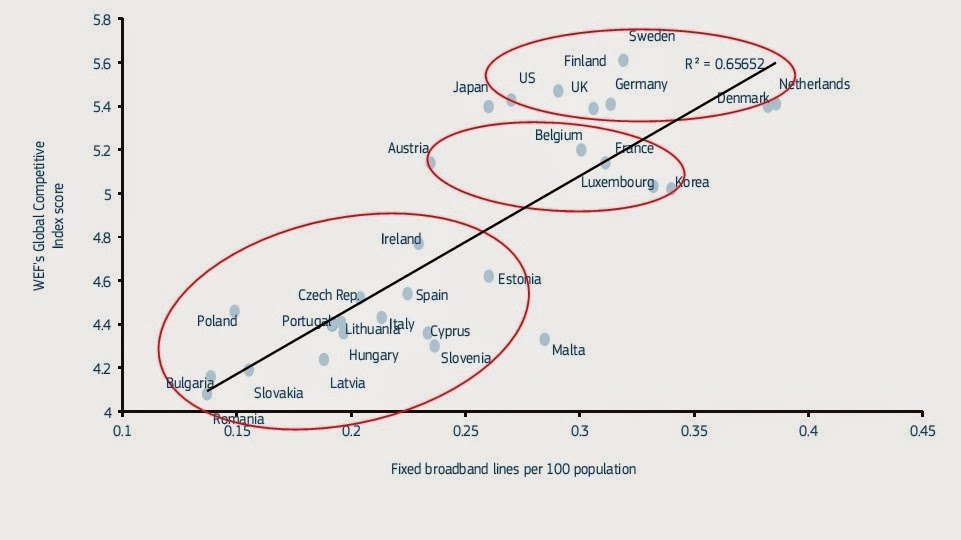

Fast and ultra-fast internet access The broadband market grew in 2011 but the growth rate continued to slow down. The fixed broadband penetration rate in January 2012 was 27.7% of the population, just 1.3 percentage points up from 26.4% in 2011. Despite the slower growth, the EU penetration rate exceeded that of Japan in 2011 for the first time. The difference with the US is 0.5 percentage points behind only. Speeds of fixed broadband lines increased significantly in 2011 w ith almost 50% of all lines providing download speeds of 10 Mbps and above. l But the take up of fast and ultra-fast broadband, i.e. 30 Mbps and 100 Mbps, is still low with just 7.2% and 1.3% (respectively) of all fixed lines providing those speeds. In the second half of 2011, the number of new broadband lines b ased on xDSL was almost equal to the number of new lines based on alternative technologies sold both by new entrants and incumbents, indicatin...